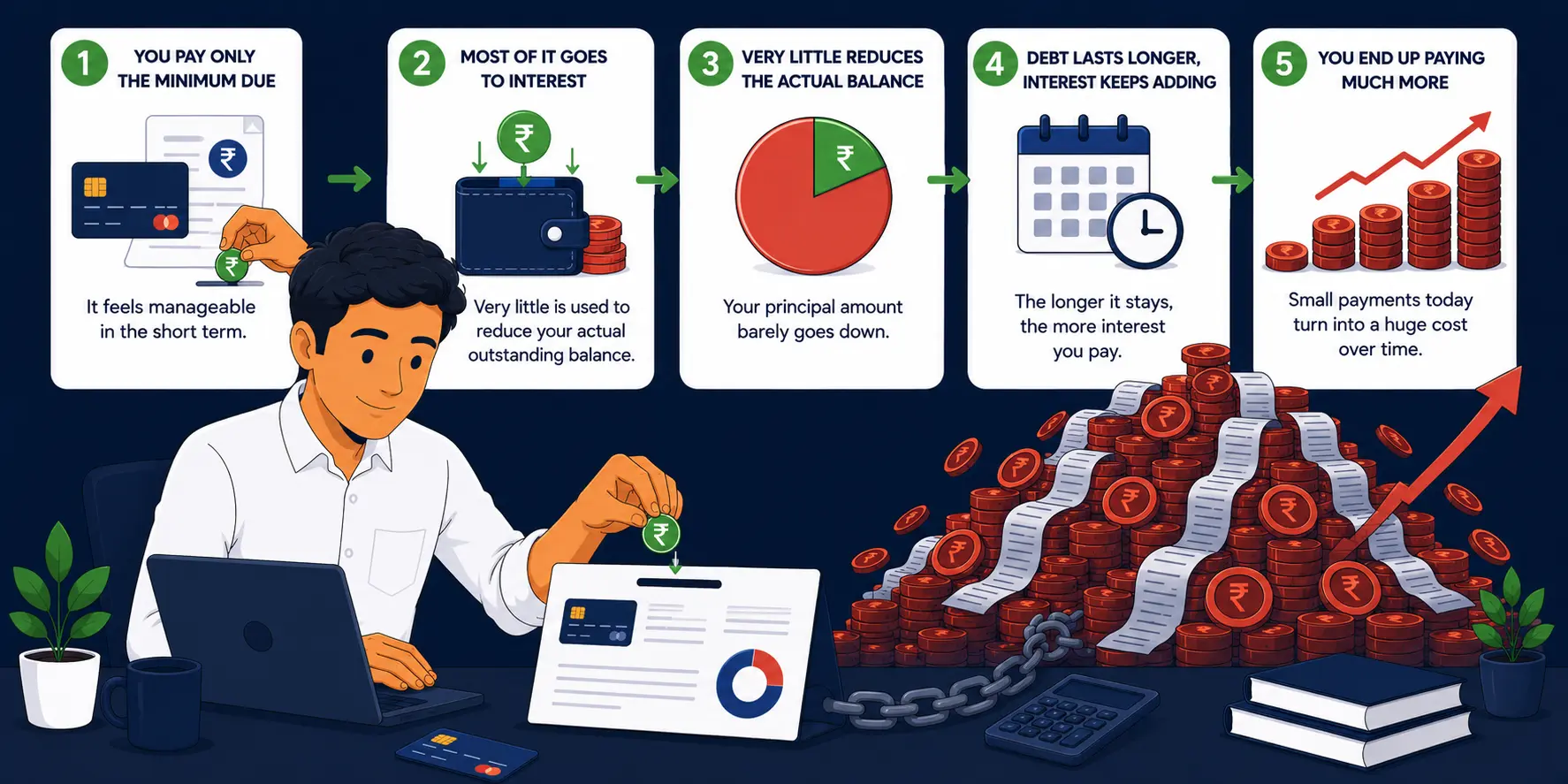

The minimum due amount on your credit card statement is one of the most cleverly designed numbers in personal finance. It is just low enough to feel manageable. Just high enough to feel responsible. And just misleading enough to keep you paying interest for years without you realising what is actually happening.

Most people who pay the minimum due are not careless. They are busy, stretched thin that month, or genuinely believe they are doing the right thing by at least paying something. That is exactly what the bank is counting on.

What the minimum due actually is

Most Indian banks set the minimum due at 5 percent of your outstanding balance or 200 rupees, whichever is higher. So if your card statement shows an outstanding of 50,000 rupees, your minimum due is 2,500 rupees.

That number looks reasonable. You pay it, the bank confirms your payment, and you feel like you handled it. What the statement does not tell you loudly is what happens to the remaining 47,500 rupees.

It starts attracting interest. Immediately. At a rate that typically ranges from 36 to 45 percent per year on Indian credit cards. That works out to 3 to 3.75 percent every single month on the full outstanding balance.

You paid minimum due of Rs.2,500

Principal actually reduced = Rs.625 only

New outstanding = Rs.49,375

You paid 2,500 rupees and your balance went down by 625 rupees. The other 1,875 rupees went straight to the bank as interest. And next month the cycle starts again on the new balance.

The mindset that makes it worse

Here is how most people think when they first pay the minimum due.

They are short on cash that month. The salary came in, rent went out, something unexpected happened. The credit card outstanding is sitting there and the minimum due feels like a lifeline. Pay this small amount, avoid a late fee, protect the credit score, deal with the rest next month when things are better.

Next month comes. Things are not dramatically better. There is a new set of expenses on the card from the current month added on top of the old balance. The minimum due is slightly higher now because the outstanding went up. But it still feels payable. So they pay it again.

And the month after that. And the month after that.

The people who pay the minimum due for one month almost always pay it for three months. The people who pay it for three months often pay it for a year. Because the circumstances that made it feel necessary the first time rarely disappear quickly. And by the time they do, the outstanding has grown and the habit is set.

What actually happens over time

Take a realistic example. You have 50,000 rupees outstanding on your card. You decide to pay only the minimum due each month. You make no new purchases on the card.

Month 1: Pay Rs.2,500. Balance becomes Rs.49,375.

Month 6: Balance is around Rs.46,800. You have paid Rs.14,400 total but your outstanding has reduced by only Rs.3,200.

Month 12: Balance is around Rs.43,900. You have paid Rs.27,600 in a year. Outstanding reduced by Rs.6,100.

At this pace, paying only minimum due, it will take you well over 8 years to fully pay off the original 50,000. And by the time you are done, you will have paid close to 1.5 lakh rupees in total for a debt that started at 50,000.

Three times the original amount. For a balance you thought you would clear in a few months.

This is not a hypothetical designed to scare you. This is the standard mathematics of revolving credit at 36 to 45 percent annual interest. The numbers work out this way every time.

Want to see exactly how long your current balance will take to clear? Enter your outstanding, your interest rate, and your payment amount to get the full month-by-month picture.

Open Credit Card Payoff CalculatorWhy the bank designs it this way

The minimum due is not a courtesy. It is a product feature designed to keep you in a revolving balance as long as possible.

When you pay the full outstanding every month, the bank earns nothing from you on interest. You are using their credit line for free and collecting reward points on top. Banks call this type of customer a transactor, and while they still make money from merchant fees, they make far more from customers who carry a balance.

A customer with 50,000 revolving at 3.75 percent monthly is generating 1,875 rupees of interest income for the bank every single month. That is 22,500 rupees per year from one customer carrying one balance. Multiplied across millions of cardholders, it is an enormous business.

The snowball effect when you keep spending

The situation described above assumes you stop using the card entirely after the initial balance. Most people do not.

They keep using the card for regular expenses because it is convenient, because they need the credit, or because stopping feels extreme. Every new purchase adds to the outstanding. The minimum due grows slowly. The interest compounds on a growing base. And the debt that started at 50,000 is now 70,000 or 80,000 even though you have been making payments faithfully every month.

This is where the confusion turns into panic. People genuinely cannot understand why the balance is not going down despite making payments every month. The answer is that the interest being added each month is outpacing the principal being reduced by their payments. They are running on a treadmill that is slowly speeding up.

If your monthly interest charge on the outstanding balance is higher than the principal portion of your minimum due payment, your balance will never reduce no matter how long you keep paying the minimum. You are paying to stand still. This happens more often than most people realise, especially at high interest rates on large balances.

How to stop the cycle if you are already in it

The first thing to accept is that paying the minimum due will not get you out. You have to pay more than the minimum every month for the balance to actually shrink meaningfully. The question is how much more and how to find that money.

The mindset shift that actually helps

Most people in a revolving balance situation feel a mix of guilt and avoidance. They know something is wrong but the full picture feels too uncomfortable to look at directly. So they keep paying the minimum, keep swiping the card, and quietly hope things will improve on their own.

They do not improve on their own. The math does not allow it.

The shift that helps is to look at the actual numbers once, clearly. What is the outstanding right now. What is the interest rate. How much is going to interest versus principal each month. How long will it take to clear at your current payment. These numbers feel uncomfortable to face but they are far less terrifying once they are visible than when they are vague.

If you have already read about how credit cards work and how the debt trap builds over time, you already understand how you got here. The next step is putting a number on it and starting to move in the other direction, one month at a time.

Use the Credit Card Payoff Calculator to see your exact payoff date, total interest cost, and how increasing your monthly payment by even Rs. 500 changes the outcome. Most people are surprised by how much faster the debt clears with a small increase.

Frequently Asked Questions

The minimum due is the smallest amount you can pay without triggering a late payment fee. It is typically 5 percent of the outstanding balance or Rs. 200, whichever is higher. Paying only this amount keeps you technically current but causes interest to accumulate on the remaining balance at 36 to 42 percent annually.

Paying the minimum due on time does not directly harm your credit score - you are meeting the payment obligation. However, carrying a high outstanding balance increases your credit utilization ratio, which does negatively affect your score. Paying the full balance every month keeps both your utilization low and your payment history clean.

For a Rs. 50,000 balance at 3.5 percent monthly interest, paying only the minimum can take 8 to 10 years to fully clear - and you end up paying nearly double the original amount in interest. The Credit Card Payoff Calculator on this site lets you enter your exact numbers and see the timeline.

Pay the full outstanding amount if you can. If not, pay as much above the minimum as you can afford - even paying 15 to 20 percent of the balance instead of 5 percent cuts the payoff time dramatically. The goal is to reduce the principal faster than interest accumulates on it.